In an increasingly digital world, fraud is evolving at a rapid pace, making it more crucial than ever for organizations to stay vigilant. Whether you’re running a small business or managing a large corporation, understanding the warning signs of fraud can save you from significant financial losses and reputational damage. This blog explores common red flags that indicate potential fraudulent activities and offers practical tips for detecting and preventing fraud before it’s too late.

Fraud can take many forms, from identity theft and credit card fraud to more sophisticated schemes like corporate espionage and insider trading. According to the Association of Certified Fraud Examiners (ACFE), organizations lose an estimated 5% of their annual revenue to fraud. With such staggering figures, it’s essential to recognize the signs early to mitigate risks effectively.

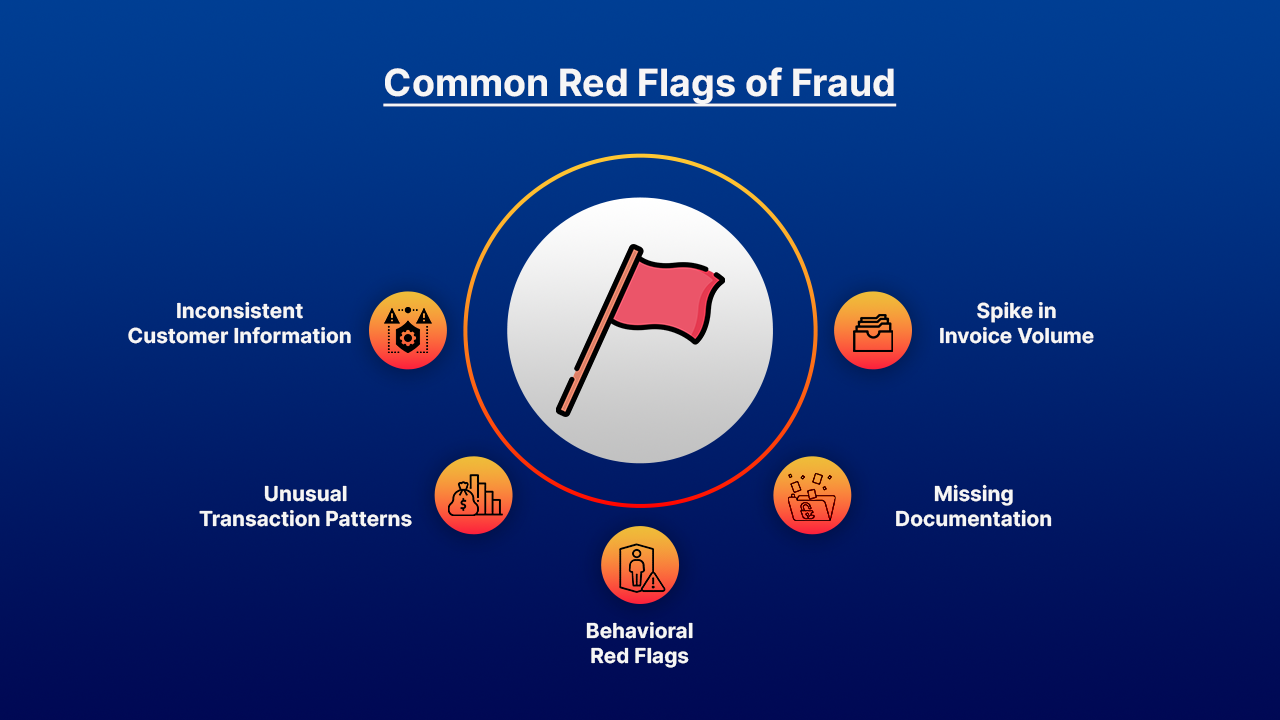

Red flags are indicators that something may be amiss. They serve as warning signs that prompt further investigation into suspicious activities. By being proactive and aware of these signs, businesses can implement measures to prevent fraud before it escalates.

One of the first places to look for fraud is in customer records. Watch for:

Monitoring transaction behaviors is crucial in identifying potential fraud:

Employees can also pose a risk when they exhibit certain behaviors:

Missing or incomplete documentation is another red flag:

Pay attention to sudden increases in invoice submissions:

Fraud is a pervasive issue that affects organizations of all sizes, with recent studies indicating that approximately 47% of businesses reported experiencing fraud in some form over the past year. According to the 2024 Global Fraud and Risk Report, the average cost of fraud per organization has risen to $1.8 million, a significant increase from previous years. Additionally, the report highlights that cyber fraud has surged by 30% as criminals exploit vulnerabilities in digital systems, making it imperative for businesses to enhance their fraud detection and prevention strategies.

Identifying red flags is just the first step; organizations must also implement strategies to detect and prevent fraud effectively.

Utilizing advanced technology can enhance your ability to detect fraud:

Regular audits are essential for maintaining oversight:

Encouraging open communication within your organization can deter fraudulent behavior:

Robust internal controls are vital for preventing fraud:

In an era where fraud tactics are becoming increasingly sophisticated, recognizing red flags is more important than ever. Common indicators—such as unexpected changes in employee behavior, discrepancies in financial records, and unusual patterns in customer transactions—can serve as early warning signs of fraudulent activity. By cultivating a culture of vigilance and encouraging employees to report suspicious behaviors, organizations can create an environment where proactive measures are taken to address potential fraud. This not only protects the company’s bottom line but also fosters trust and integrity within the workplace.

Fraud may be pervasive, but it doesn’t have to be inevitable. By recognizing the common red flags and implementing proactive measures, organizations can significantly reduce their risk exposure. Staying vigilant and fostering a culture of transparency are key components in the fight against fraud.

As we navigate through an increasingly complex landscape, remember that awareness is your best defense. By educating yourself and your team about potential warning signs and taking decisive action when necessary, you can protect your organization from the devastating effects of fraud. If you're looking for tailored solutions or need assistance in enhancing your fraud detection strategies, contact us today! Our team of experts is here to help you build robust systems that safeguard your organization against potential threats while fostering a culture of integrity and transparency.

In our newsletter, explore an array of projects that exemplify our commitment to excellence, innovation, and successful collaborations across industries.